UNPACKING INNOVATIONS 001: A DEEP DIVE INTO RIBH FINANCE

Overview of Ribh Finance

Ribh Finance, pronounced [rɪbɑː], means profit or gain (ربح) in Arabic — I didn’t know either until Startup Village where SuperteamNG Lagos’ Writer’s Lead, Lili and Emeka Nwosu, the founder and COO, spoke about it on Day 1.

So, what is Ribh Finance really?

It’s a financial platform leveraging stablecoins (USDC) on Solana to tackle deep-rooted payment inefficiencies for SMEs in emerging markets, particularly across Africa and Latin America. Their mission is bold but simple: Enable seamless, low-cost, and stable transactions for businesses plagued by currency volatility, high banking fees, and outdated payment rails — everything Web2 banks and FinTechs couldn’t fix.

Basically, they’re rewriting everything Web2 banks and FinTechs got wrong about cross-border payments — and doing it with Web3 tools.

Sounds like a big claim. Are they actually pulling it off? Oh, absolutely. Let’s talk numbers. On March 26, 2025, Ribh hit $4.1M in Total Volume Processed (TVP). By April 14, that number jumped to $6.1M. That’s 48.8% growth in just 42 days.

Let me break it down for you:

India’s UPI — the most dominant payment system in the world’s most populated country — saw 90% YoY growth in 2022. If you linearize that, it’s about 30% over 42 days. Now compare that to Ribh’s 48.8%, as a single startup, in less than two months. That’s unheard of in banking and FinTech history.

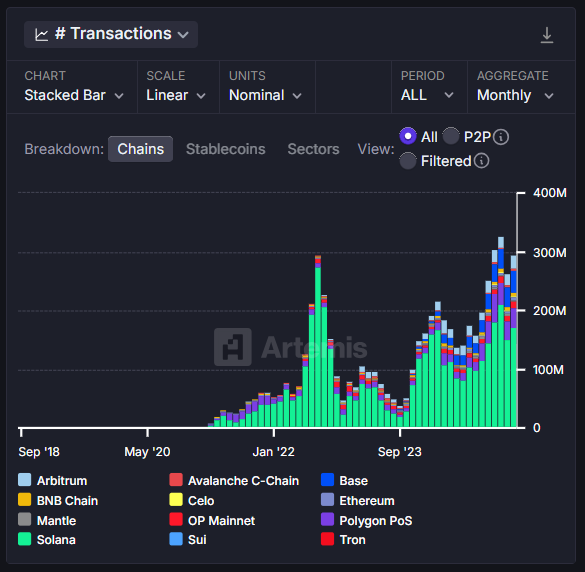

But wait — why Solana? Let’s be real. You can talk about “low fees and fast transactions” all day but if you’re building on a blockchain that drops new L2s every week just to fix itself, you’re probably not fixing anything.

Ribh needed speed, low-cost, and stability. So naturally, they built on Solana. Here’s what most don’t realize: Solana is USDC’s most promising blockchain. Not by total supply — that’s vanity. By real usage:

Highest active addresses

Most transactions

Fastest growth in stablecoin adoption

(Credits to Artemis Analytics for backing this with real data, not vibes.)

USDC Transactions and Active Addresses;

Reflect user adoption and engagement,

Less susceptible to skew from large transactions,

Indicate cost-effectiveness and accessibility,

Better capture organic and retail activity and,

Forward-looking indicators of growth potential.

Ribh Finance isn’t just another startup, it’s a statement.

Core Problems Ribh Finance Solves

Small and Medium-sized Enterprises (SMEs) in emerging markets have long been underserved by traditional finance. From high fees to currency instability and snail-paced cross-border transactions, the system is rigged against the people trying to build real businesses. Ribh Finance exists to flip that narrative. Let’s unpack the pain points and how Ribh is tackling each one head-on.

1. High Payment Fees

Every time a payment is made, a chunk of the money is shaved off as fees — not because anyone’s trying to rob you, but because too many middlemen want a cut. Here’s how it typically breaks down:

A portion goes to the issuing bank

Another cut is taken by the payment processor

FinTech programs and BaaS providers also take their share

Before the money reaches its destination, everyone’s dipped their hand in the pot.

Banks remain the most expensive option for cross-border transfers, charging an average of 11.48%. In fact, Sub-Saharan Africa is the most expensive region in the world to send money to, with average costs at 7.73% in Q1 2024, according to the World Bank. That’s way above the global average of 6.35% — and it hits small businesses the hardest.

2. Currency Volatility

Currency fluctuation doesn’t just mess with your books — it can break your entire business model.

Take Nigeria for example. On February 22, 2024, the Naira dropped to an intraday low of ₦1,851 per dollar, down from ₦1,571–₦1,600 the day before.

Let’s say you’re a small business owner paying your supplier in China $3,000. You make the payment on February 21 at ₦1,571 per dollar — that’s ₦4,713,000. But by the time it gets processed the next day, the exchange rate has tanked, and your supplier ends up receiving just $2,546.19.

That’s a shortfall of nearly $454 — and you’re the one who has to cover it.

3. Slow and Cumbersome Banking

The traditional system wasn’t built for us — and it shows.

Back in 2017 when I started freelance writing on Fiverr, I couldn’t even receive basic $10–$50 payments. I had to do a workaround — pay someone else for a gig, and they’d send me the Naira equivalent.

Tried PayPal? Not available for Nigerians. So I had to send payments to someone else's PayPal and lose a chunk to “fees.”

Payoneer? Great — but you needed to hit a minimum withdrawal limit. Then came the never-ending bank processes:

Fill a form to withdraw

Wait several business days

Get flagged

Fill another form

Wait again

And that's after you've already worked for the money.

Now imagine you’re a business owner trying to send or receive payments across borders. It’s more than frustrating — it’s a major bottleneck.

To make matters worse, Africa’s regulatory landscape is fragmented, with each country enforcing different rules on:

Foreign exchange

Anti-money laundering (AML)

Transaction reporting

This fragmentation makes true regional integration a nightmare.

How Ribh Finance Fixes This

1. Stablecoins (USDC)

Ribh Finance lets businesses transact using USDC, a dollar-pegged stablecoin. This removes the chaos of currency swings.

So whether the Naira, Colombian Peso, or Brazilian Real is crashing, your payment stays solid. You’re dealing in dollars — accepted globally, respected everywhere.

2. Low-Cost Transactions

Ribh is built on Solana, which means:

Blazing fast transaction speeds

Sub-cent fees

This isn’t just a financial service — it’s financial freedom.

3. No Volume Restrictions

Whether you're sending $100 or $1,000,000, Ribh doesn’t penalize you based on size. There are no minimums, no hidden clauses — just clean, borderless payments.

Key Features

Peer-to-peer (P2P) commerce using stablecoins

No intermediaries, which slashes costs

Built specifically for SMEs in Africa and Latin America

The Bigger Vision

One platform for global payments and global visibility.

Ribh Finance isn’t patching the holes in the system — it’s building a new one entirely. One where small businesses in Lagos, Bogotá, or São Paulo can access the same financial tools as those in New York or London.

And this time, it actually works.

Growth & Milestones

Ribh isn’t just talking the talk — it’s putting in the work and making waves.

As a key contributor to Solana’s growing stablecoin adoption across Africa and Latin America, Ribh is proving that impactful innovation can come from — and scale within — emerging markets.

In the Colosseum Radar Hackathon, Ribh secured 4th place in the Payments Track, standing out among:

10,000+ participants

1,359 product submissions

From over 120 countries

That’s not just a win — it’s a statement.

In terms of traction, Ribh has seen impressive growth:

As of March 26, 2025, it had processed $4.1M in total volume

By April 14, 2025, that number jumped to $6.1M

That’s nearly $2M in growth in less than 3 weeks — proof that there’s real demand for a product that actually solves the right problems.

Founder’s Vision: Nwosu’s Insights

At the SuperteamNG Startup Village Pitch, Emeka Nwosu, the founder and COO of Ribh Finance, delivered more than just a pitch — he shared a mission.

Ribh was introduced as a platform built for real-world commerce, designed to bring stable, instant, and low-cost financial services to the businesses that need them most — SMEs in emerging markets.

Their product suite includes an app and a plug-and-play widget that empowers businesses to:

Receive payments in their local currency

Instantly convert those payments to USDC

Automatically swap USDC to their own local fiat

All this is made possible by Ribh’s active trade desk, which handles bulk swaps and conversions behind the scenes — allowing businesses to focus on selling, not settlement delays. This is next-gen payment collection and invoice infrastructure — tailor-made for the volatility and fragmentation of emerging market economies.

But Ribh isn’t stopping there.

Introducing De Ahia — which translates to "The Market" in Igbo — a decentralized marketplace rooted in Igbo culture and inspired by the spirit of open trade. It’s a peer-to-peer commerce platform powered by stablecoins, enabling users to:

List products

Trade directly

Connect with global buyers.

No middlemen, just real trade and real value, across borders and blockchains.

Nwosu’s vision is clear: financial freedom, built for the people, with the people in mind.

Conclusion

Ribh Finance is doing more than just connecting crypto with real-world commerce — it’s actively empowering SMEs in volatile economies across Africa and Latin America. From De Ahia, their decentralized marketplace, to their rapid TVP growth and visionary leadership, Ribh is carving out a role as a core player in stablecoin-powered trade.

But let’s be clear — Ribh Finance isn’t just building a wallet. It’s building a full commerce infrastructure, forming partnerships with merchants and liquidity providers to unlock seamless payments, instant settlements, and borderless opportunities.

Even if you’re not into business, not into selling or trade — you buy things, you send money, you make payments. And for that, you benefit from what Ribh is building. Because Ribh Finance is not just another Web3 payments startup. It’s a mission-driven platform rethinking how money moves in emerging markets — replacing volatility with stability, delays with speed, and inefficiency with execution.

In a space full of dreamers and theorists, Ribh is a doer — backed by numbers, growth, and relentless delivery. Web3 isn’t waiting for the future, Ribh is already fixing what’s broken — right now. Follow Ribh Finance and keep an eye on De Ahia. The next wave of financial freedom for emerging markets is already in motion — and it’s only just getting started.

Reference

Nwosu’s interview at SuperteamNG Startup Village